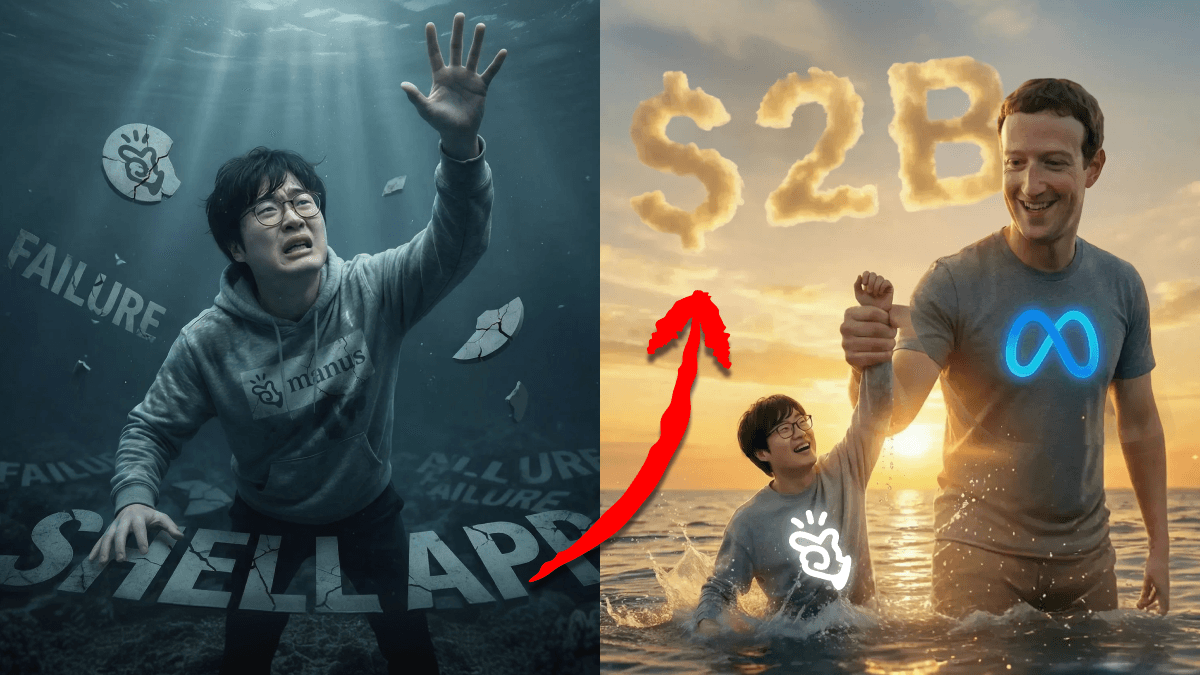

Meta's $2 Billion Manus AI Acquisition: From 'Shell Product' to Mega Exit

Steve Oak (Okkar Kyaw)

TLDR

Manus AI went from being called a "shell product" with "unusable" software to a $2 billion Meta acquisition in just nine months. This is the fastest failure-to-acquisition story in AI history, and it reveals why the shift from chatbots to AI agents is reshaping Big Tech strategy.

Prefer Video Experience? Watch below 👇

Prefer Audio Experience? Listen below 👇

The Demo That Broke the Internet

March 2025. Manus drops a demo that sets the AI world on fire. It's positioned as the first "general AI agent" - an AI that actually does things, not just talks about them. You give it a task, watch it plan, execute, and deliver real results. No wall of text. Actual output.

The hype was immediate and intense. Invite codes were selling for $14,000 on Xianyu (China's secondary marketplace). People were calling it the next DeepSeek moment. The transparency layer - where you could see every action the agent takes - was genuinely innovative.

The key differentiator: "The AI that DOES" became Manus's viral tagline, separating it from the sea of chatbots that merely respond.

But here's the thing about hype. It's a loan you have to pay back with results. And Manus was about to default.

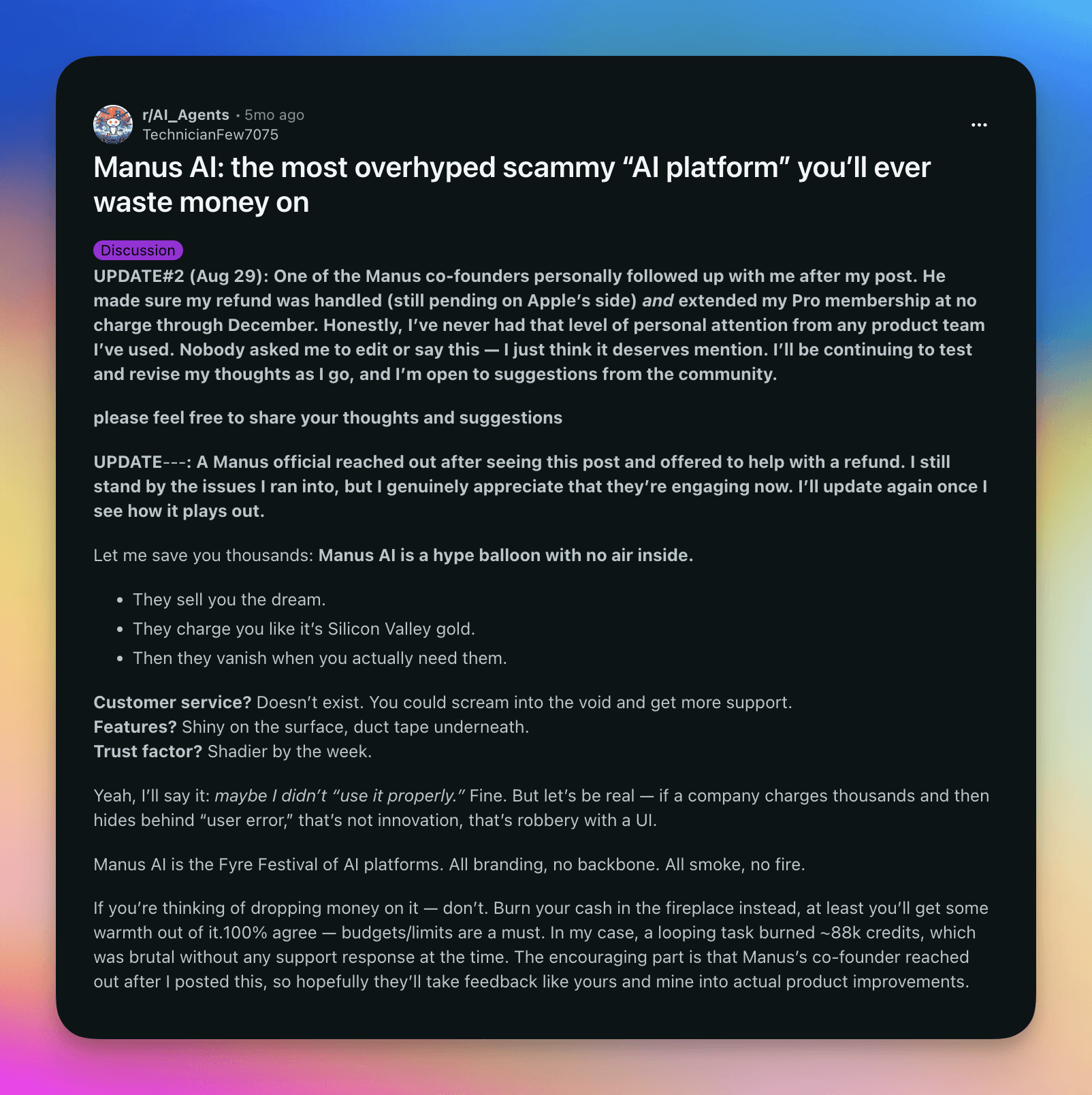

The Brutal Backlash

Chinese social media turned hostile fast. The accusations were brutal:

"Pure shell product" - just a wrapper on Claude with nothing original

"Hunger marketing. Did they just raise money and run?"

Users losing 800 credits uploading a single file

Reddit threads calling it "absolutely unusable"

Most startups die at this stage. Once the "scam" narrative takes hold, you can't outmarket your way out of it. The product had real problems, and the court of public opinion had already rendered its verdict.

But Manus didn't die. They made a critical pivot that would change everything.

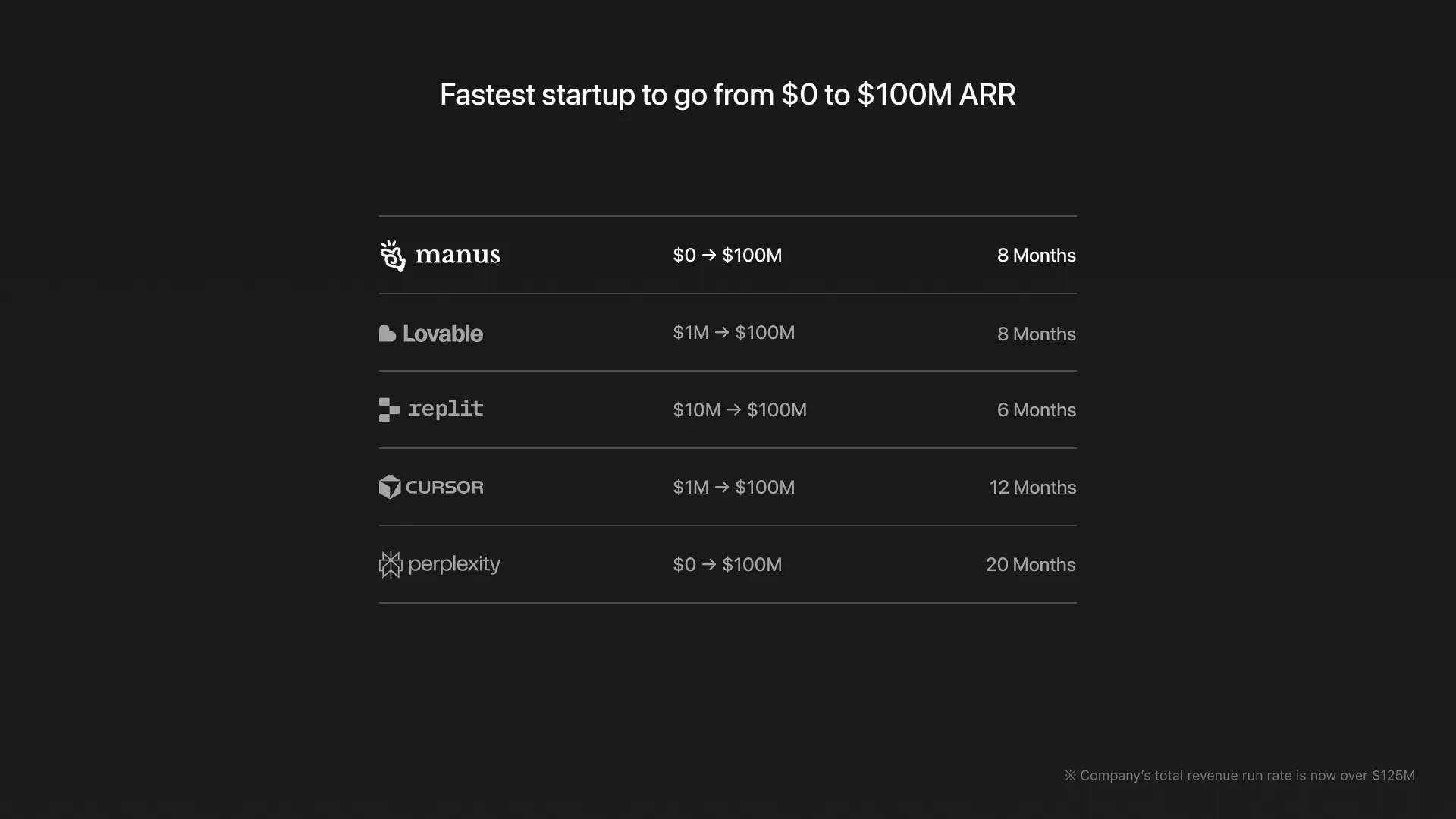

The $100 Million Resurrection

Instead of chasing Twitter virality, Manus started chasing invoices. They went heads-down on product.

June 2025: Playbook templates launched - pre-built task flows that cut credit consumption by 30%.

July 2025: Chat Mode introduced - simple queries now used 5 credits instead of 100. The product became actually usable.

Then the enterprise deals started landing:

Client | Use Case | Result |

|---|---|---|

Mercury Law (UK) | Contract review | 40% time savings |

Shanghai Zenith Advertising | Campaign automation | Reduced manual work |

Beijing consultancies | Research workflows | Faster client delivery |

Real companies. Real invoices. Real validation.

By December 2025: $100 million ARR. Two million users. From "shell product" to nine-figure revenue in six months.

That's not a pivot. That's a resurrection.

Why Meta Paid $2 Billion in 10 Days

Normal M&A takes months of due diligence. Meta closed in 10 days. That's not strategic - that's desperation.

Here's the competitive landscape Meta was facing:

Google: Gemini Agents rolling out across Workspace

Microsoft: Copilot embedded everywhere

OpenAI: Function-calling agents shipping rapidly

Anthropic: Claude becoming the go-to for agentic workflows

Everyone was moving. Meta was stuck.

The real story: Meta is quietly shifting away from open source. They're building a proprietary model codenamed "Avocado." The "Llama is free forever" era is changing. They need revenue from AI, not just developer goodwill.

Meta didn't just buy revenue. They bought an agentic architecture they were years behind on building themselves. According to Gartner, 40% of enterprise apps will have AI agents by end of 2026 - up from 5% the year prior.

The shift is happening fast. Meta paid $2 billion to be on the right side of it.

The Bigger Picture: Chatbots Are Dead

This acquisition isn't just a Manus story. It's a signal about where AI is heading.

Chatbots chat. Agents act.

The difference is fundamental:

Chatbots | AI Agents |

|---|---|

Respond to prompts | Execute multi-step tasks |

Generate text | Deliver outcomes |

Require human orchestration | Operate autonomously |

Useful for Q&A | Useful for work |

The transparency layer that Manus pioneered - watching the AI think, plan, and execute in real-time - that's becoming table stakes. Users want to see the work happening, not just get a text response.

Key Takeaways

The Manus story offers several lessons for anyone watching the AI industry:

Product beats narrative: All the viral marketing couldn't save Manus when the product failed. Only fixing the product did.

Enterprise revenue validates: $100M ARR in six months turned "shell product" criticism into a $2B exit.

Timing matters: Meta was behind on agents precisely when the market shifted from chatbots to agents.

Speed signals desperation: 10-day M&A cycles don't happen unless someone is scared of being left behind.

From shell product to $2 billion in 9 months. Failure to acquisition. Hate to exit.

That's the Manus story.

Frequently Asked Questions

What is Manus AI and why did Meta acquire it?

Manus AI is a Chinese startup that built one of the first "general AI agents" - software that executes tasks rather than just responding to prompts. Meta acquired Manus for $2 billion to quickly gain agentic AI capabilities they were behind on developing internally.

How much did Meta pay for Manus AI?

Meta paid $2 billion for Manus AI in a deal that closed in just 10 days - unusually fast for tech M&A of this size.

What's the difference between AI agents and chatbots?

Chatbots respond to prompts with text. AI agents execute multi-step tasks autonomously. Chatbots tell you how to do something; agents actually do it for you.

Why was Manus AI called a "shell product"?

Critics on Chinese social media accused Manus of being just a wrapper on Claude (Anthropic's AI) with no original technology. The product also had usability issues, including excessive credit consumption for basic tasks.

How did Manus go from criticism to $2 billion exit?

Manus pivoted from chasing viral marketing to building enterprise value. They fixed product issues, launched cost-saving features like Playbook templates and Chat Mode, and landed major enterprise clients. Revenue growth ($100M ARR by December 2025) validated the business despite earlier criticism.

" height="27.75px" id="uLviGCnmH" width="32.250290101110345px"/></svg>)

" height="30.750000122616527px" id="vGhZKbMSS" width="30.75px"/></svg>)

" height="30.750000122616527px" id="TPi0p5D9h" width="30.75px"/></svg>)

" height="30.750000122616527px" id="fXIphKa5h" width="30.75px"/></svg>)